Comparison · 2026

TIAA vs Fidelity & Vanguard

The “best” provider depends on what your plan offers and what you value. Here’s the plain comparison.

Important: This is independent educational information only. It is not financial advice, and Elmscotton is not affiliated with or endorsed by TIAA. Confirm the rules for your own contract and consider a licensed advisor before acting.

TIAA vs Vanguard

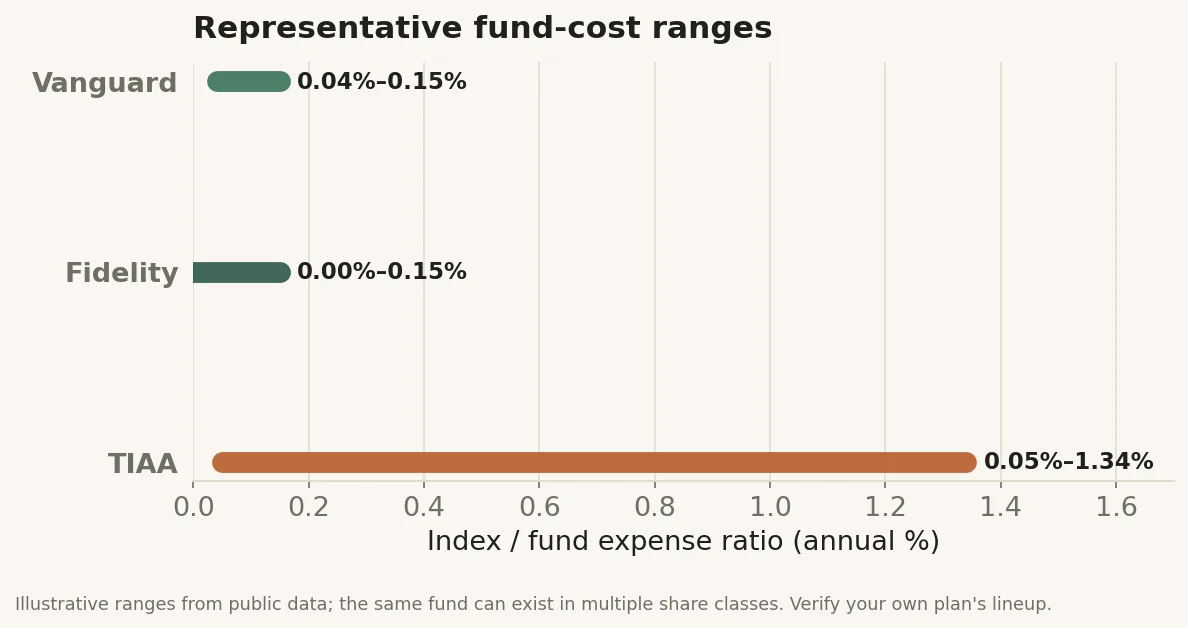

Vanguard pioneered low-cost indexing and is widely seen as the cost leader; a simple three-fund portfolio there is hard to beat on price. TIAA’s edge is the Traditional Annuity’s guarantee and income options. No need for those? Vanguard is usually the cheaper long-term home for index money.

TIAA vs Fidelity

Fidelity offers very low-cost index funds (including some zero-expense-ratio funds), broad choice and strong support, and like TIAA often runs on-campus sessions. For index-focused educators it generally beats TIAA’s pricier share classes on cost.

Practical step: list every fund you hold and its expense ratio, then compare to a broad index equivalent. The provider name matters less than the specific share classes available to you.