In-depth Review · 2026

TIAA 403(b) review 2026: is it still worth it?

For most teachers and professors, TIAA is the 403(b) — it has been the default since 1918. In 2026, with low-cost rivals everywhere, here’s an honest read on whether it still earns its place.

The verdict in one paragraph

If you value a guaranteed floor under part of your savings and optional lifetime income, TIAA’s Traditional Annuity is something most 403(b) menus can’t replicate. If you simply want the cheapest index investing with full flexibility, a plan with Vanguard or Fidelity options usually wins on cost. Blending the two is often the smartest move.

The Traditional Annuity, briefly

TIAA Traditional is a guaranteed-interest insurance contract — not a market fund. It credits a guaranteed minimum (historically ~3% on classic RA/SRA contracts, as low as 1% on newer RC contracts) plus possible extra amounts that aren’t guaranteed for the future. The catch is liquidity: in RA contracts you generally can’t take a lump sum, and money leaves through a multi-year Transfer Payout Annuity.

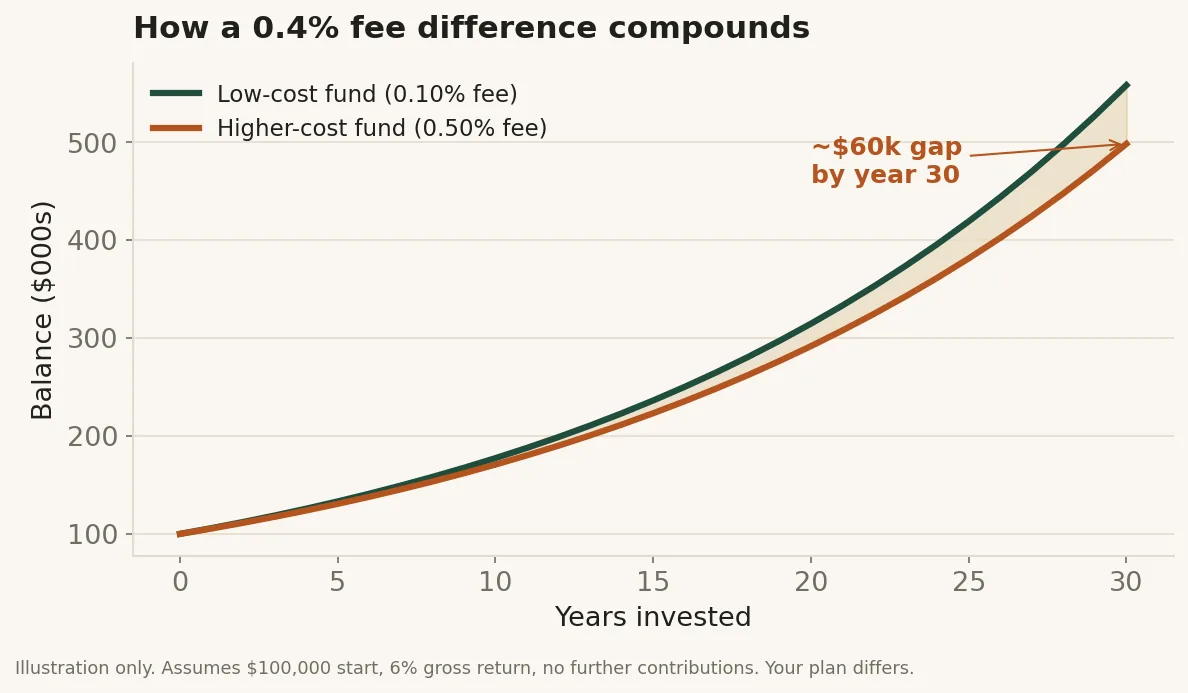

Fees: check your share class

TIAA’s costs are inconsistent. Some index funds are cheap; some proprietary and active funds have charged far more than comparable funds elsewhere — and the same fund can sit in a pricier share class. A 0.3% difference sounds tiny but compounds into thousands over a career. Run your own numbers.

Good fit / poor fit

- Good fit: savers who want a guaranteed floor and pension-like income, and value stability over the last basis point.

- Poor fit: DIY index investors who want rock-bottom fees and full liquidity, especially if their plan offers cheap Vanguard/Fidelity options.